5 Top CRE Opportunities in the Midst of Pandemic

Historically, during times of major distress there are unexpected investment opportunities that arise – the COVID-19 pandemic is no exception. At this point in the disaster’s cycle, it is important to evaluate the data, developing a statistical analysis that breaks down the future value of specific sectors. Here are five asset classes that we have recognized as top CRE opportunities in the midst of this pandemic.

Multifamily

Multifamily has proven to be the most resilient of the asset classes.

According to the National Multifamily Housing Council, the rate of Class A renters who have paid their rent on time has remained stable over the last three months, whereas Class B/C have fallen:

| City | May 1-13 | June 1-13 | July 1-13 |

|---|---|---|---|

| Class A | 84% | 90% | 84% |

| Class B | 83% | 90% | 82% |

| Class C | 73% | 84% | 69% |

Secondary Cities

Secondary cities, those with populations below 500,000 people, are drawing an increasing number of white-collar workers searching for a lower cost of living, smaller tax burden, job growth, and affordable housing.

Markets outside of the core coastal markets are significantly more affordable, with many rent-to-income ratios below 0.30, as seen in Figure 1.

| City | Average Income | Average Monthly Rent | Rent to Income Ratio |

|---|---|---|---|

| Charlotte, NC | $73,202 | $1,515 | 0.25 |

| Austin, TX | $98,124 | $2,046 | 0.25 |

| Jacksonville, FL | $67,232 | $1,572 | 0.28 |

| Atlanta, GA | $73,251 | $1,744 | 0.29 |

| Nashville, TN | $70,384 | $1,171 | 0.30 |

According to the online consumer real estate platform Redfin, the highest percentage of Atlanta’s and Nashville’s new residents are from New York City. New residents in Phoenix, Dallas, and San Diego are mostly from Los Angeles; Portland’s and Austin’s new residents are primarily from San Francisco.

“People in the coastal markets are just fed up with double-digit price increases, and they’re moving to a commuter town or to the middle of the country,” said Daryl Fairweather, Redfin’s chief economist in an interview with The Washington Post.

The acceleration of the work-from-home trend due to coronavirus-forced business closures and social distancing practices has led to a nationwide awakening among knowledge workers that they don’t need to make the daily commute to and from an office location in a large city.

A recent Gallup poll found that as states lift public health restrictions:

- 62 percent of employed Americans are working from home—double since mid-March

- 59 percent prefer to continue to work remotely as much as possible

- Only 41 percent want to return to their workplace or office, as they did before the crisis

Whether or not they work from home, reducing their overall exposure to the coronavirus and future virus outbreaks is another driver of this trend. Secondary cities have reported much lower numbers of coronavirus infections and COVID-19 patient hospitalizations than the country’s largest cities. They are less densely populated, attract far fewer tourists, often do not serve as international travel hubs, and have fewer public transportation options than larger cities.

It’s important to note that the pandemic remains virulent and unpredictable. As of this writing, the numbers of new cases in cities and states that recorded higher infection rates in the early days of the outbreak have declined, but the opposite is true for regions that previously had lower rates of infection.

Single-Family Rentals

The rising delinquencies in rent payments nationwide, high unemployment, and consumers’ anxieties over job instability will likely compel would-be home buyers to continue renting. But that won’t prevent them from trying to secure the space and stability that a single-family home offers. SFR rent collection has actually been stronger than Multifamily, with about 5 percent uncollected.

According to Jeff Cline of SVN/SFRhub Advisors, demand for single-family portfolios, defined as five or more homes, has skyrocketed in the last month, up 650 percent. That is spurring leasing companies like Invitation Homes, the country’s largest single-family landlord, to expand their portfolios of single family rentals. Invitation Homes raised $448 million in a share sale in June and reportedly plans to use a bulk of the proceeds to buy more properties.

According to John Burns Real Estate Consulting, the single-family rental space was the first to experience more robust demand after the pandemic struck as apartment residents and city dwellers sought out larger spaces. Most operators reported an uptick in demand during the last two weeks of March.

“Single-family rentals allow financial flexibility (no need to qualify for a loan, no down payment, no 30-year mortgage) and privacy, with enhanced social distancing opportunities for residents,” added Ken Perlman and Lesley Deutch, both Managing Principals at John Burns. “Often, they are renters by choice and will pay a premium to live in a dedicated community with other renters and community amenities rather than in a privately owned rental home.”

Since the pandemic struck in mid-March, the hardest-hit markets from an economic perspective have been those with a concentration of services workers, such as Las Vegas and Honolulu.

ECONOMIES WITH THE LARGEST CONCENTRATION OF SERVICES WORKERS

% Percent of Jobs in Hardest Hit Services Categories

| Top 10 (Most Impacted) | Bottom 10 (Least Impacted) | ||||

|---|---|---|---|---|---|

| 1. | Las Vegas, NV | 38.50% | 1. | Raleigh, NC | 13.51% |

| 2. | Honolulu, HI | 32.75% | 2. | Pittsburgh, PA | 13.55% |

| 3. | San Antonio, TX | 30.48% | 3. | Milwaukee, WI | 14.39% |

| 4. | San Bernardino, CA | 27.70% | 4. | Boston, MA | 14.43% |

| 5. | Virginia Beach, VA | 26.24% | 5. | Detroit, MI | 14.78% |

| 6. | Orlando, FL | 25.73% | 6. | Charlotte, NC | 14.93% |

| 7. | Sacramento, CA | 25.36% | 7. | San Jose, CA | 15.26% |

| 8. | Columbus, OH | 22.69% | 8. | Indianapolis, IN | 15.64% |

| 9. | Tampa, FL | 22.53% | 9. | Providence, RI | 15.73% |

| 10. | Denver, CO | 22.15% | 10. | St. Louis, MO | 15.88% |

An institutional investor’s focus should be on markets whose economies are well-insulated from future shut-downs. Secondary cities like Raleigh and Pittsburgh with large percentages of white collar workers will continue to thrive. Employees can work from home, indefinitely if need be, and these cities offer more affordable “office space” than Manhattan or San Francisco.

Last-Mile Industrial

The pandemic has dramatically impacted the retail and restaurant sectors, forcing consumers to change how they approach shopping. Why expose themselves to health risks by browsing store aisles or spend time waiting in curbside pickup lines when they can buy virtually anything online and have it delivered to their doors?

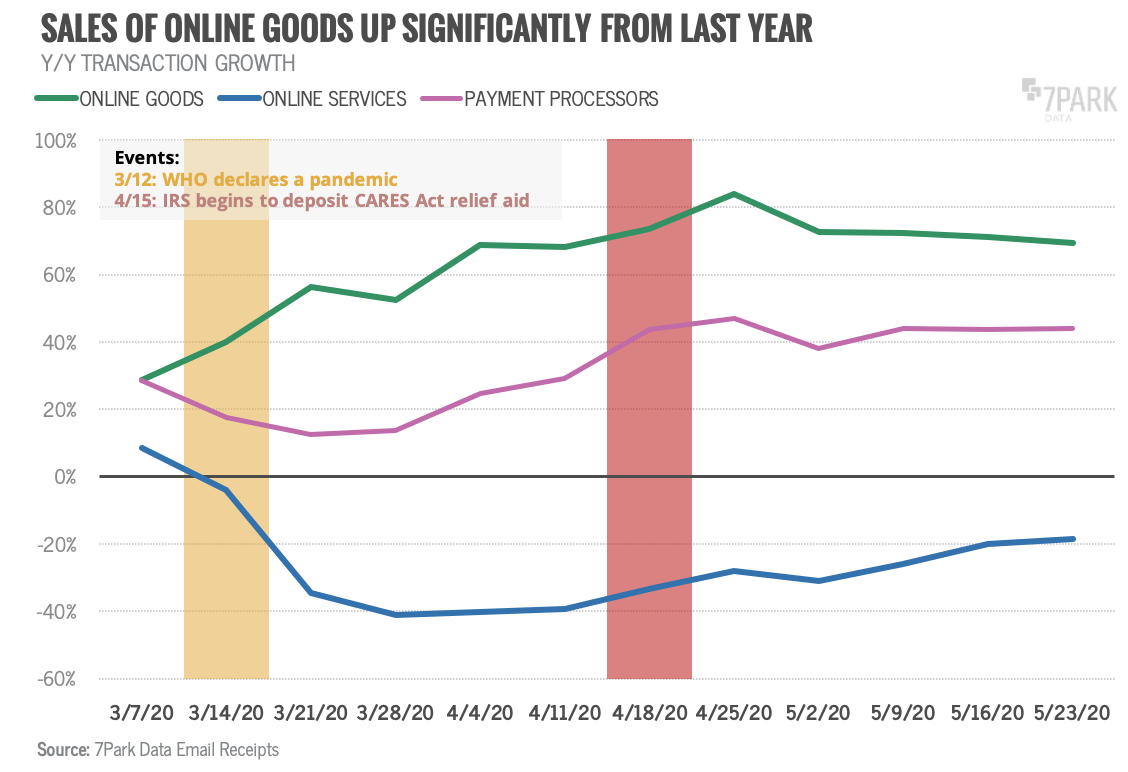

As a result, online shopping’s popularity has exploded (Figure 3). Retailers have invested heavily in opening new warehouses and distribution centers to speed the delivery of products as they travel the crucial “last mile” to the consumer.

Of course, online sales will decelerate as states lift health restrictions and allow brick-and-mortar stores to re-open. For the week of June 6, online goods order growth was over 54 percent, down from over 65 percent the previous week and over 85 percent from its April 25 peak. All product categories experienced sales declines—except one.

Grocery-Anchored Retail Stores

Supermarkets were deemed essential and permitted to remain open, rewarding investors who bet on grocery-anchored retail locations. But that did not discourage consumers from doing their grocery shopping at home.

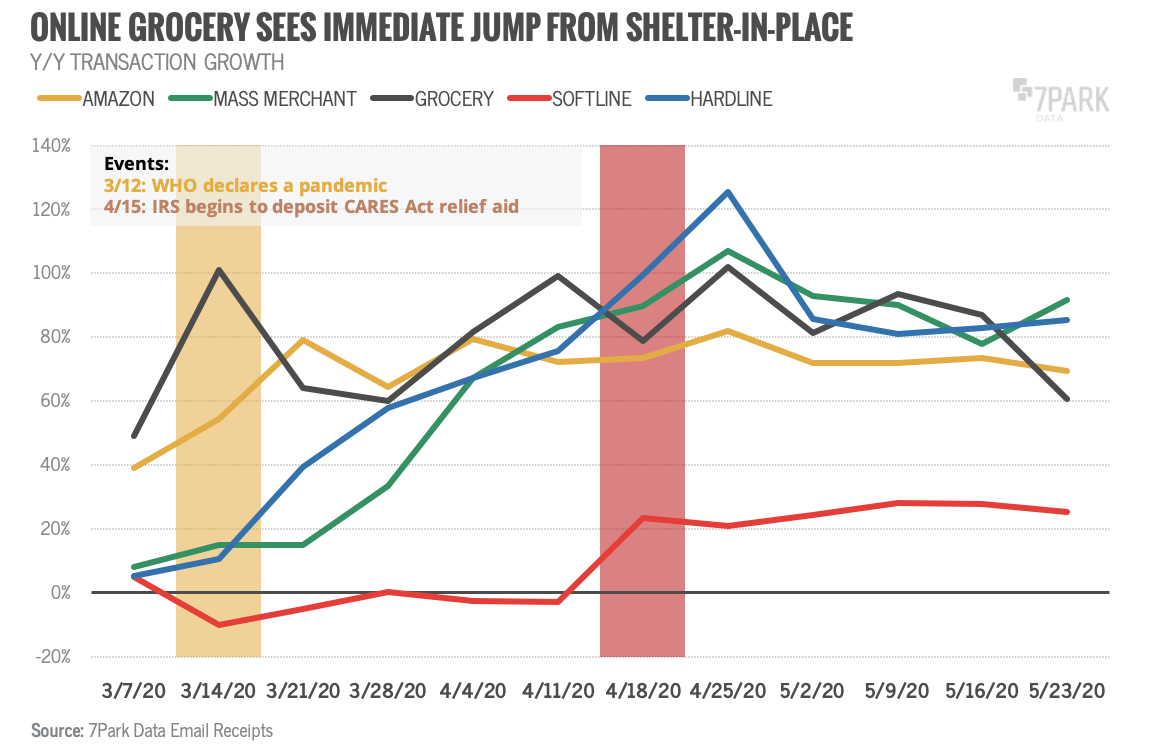

Online grocery sales have posted triple-digit order growth since the onset of the pandemic in mid-March. Grocery and other food merchants (including pet supplies) were up 110 percent for the week of June 6, flat from the previous week (see Figure 4).

Grocers will look to create facilities exclusively for delivery in addition to their in-store models. Therefore, cold-storage has and will continue to be an excellent opportunity for institutional investors. An entirely new CRE sector may emerge for online grocery delivery that eliminates pick-and-delivery from brick-and-mortar locations.

Coronavirus infection rates are rising in the majority of states, ensuring that the pandemic, and its impact on the nation’s economy, will drag on through at least the remainder of 2020. While Congress deliberates the next stimulus package, millions of renters face the threat of eviction, the unemployment rate will likely rise as businesses that opened are forced to close again, and students K-12 and in college will have to attend classes from home. Yet as the old saying goes, “the numbers don’t lie.”

With challenges come opportunities, and the current circumstances are no different. To identify and capitalize on attractive investments, commercial real estate professionals need to leverage diverse datasets (about hiring, consumer spending, permitting, demographics, etc.) and data-science powered tools to create actionable insights that are relevant today, not based on six month old news. Adding data-based insights to the tremendous amount of human capital and expertise in the commercial real estate industry will allow investors to go beyond the five opportunities outlined here and find their own unique investment thesis.

About the Author

Some Related Posts

-

QuadReal Property Group Provides $64M Refi for Mississippi State Student Housing Community

Institutional capital continues to show confidence in the student housing s -

Citadel Pivots in Miami, Drops Hotel for Offices

Citadel is reinforcing its long-term commitment to Miami with a revised hea -

March 1, 2024

March 1, 2024How to Effectively Predict and Respond to Commercial Real Estate Cycles

The commercial real estate (CRE) market, like many other financial sectors, -

January 8, 2024

January 8, 202410 Things You Should Know About Biden’s Office to Residential Conversion Plan

The Biden Administration has recently unveiled an ambitious plan aimed at a -

September 26, 2023

September 26, 2023Another Government Shutdown Is Looming – How Will this Affect the Real Estate Market?

The US has experienced several government shutdowns in recent years, often